2025 Student Housing Market Update

The student housing market in 2025 faced a tight supply-demand balance with rising rents, steady enrollment growth, and declining new bed deliveries. Key highlights include:

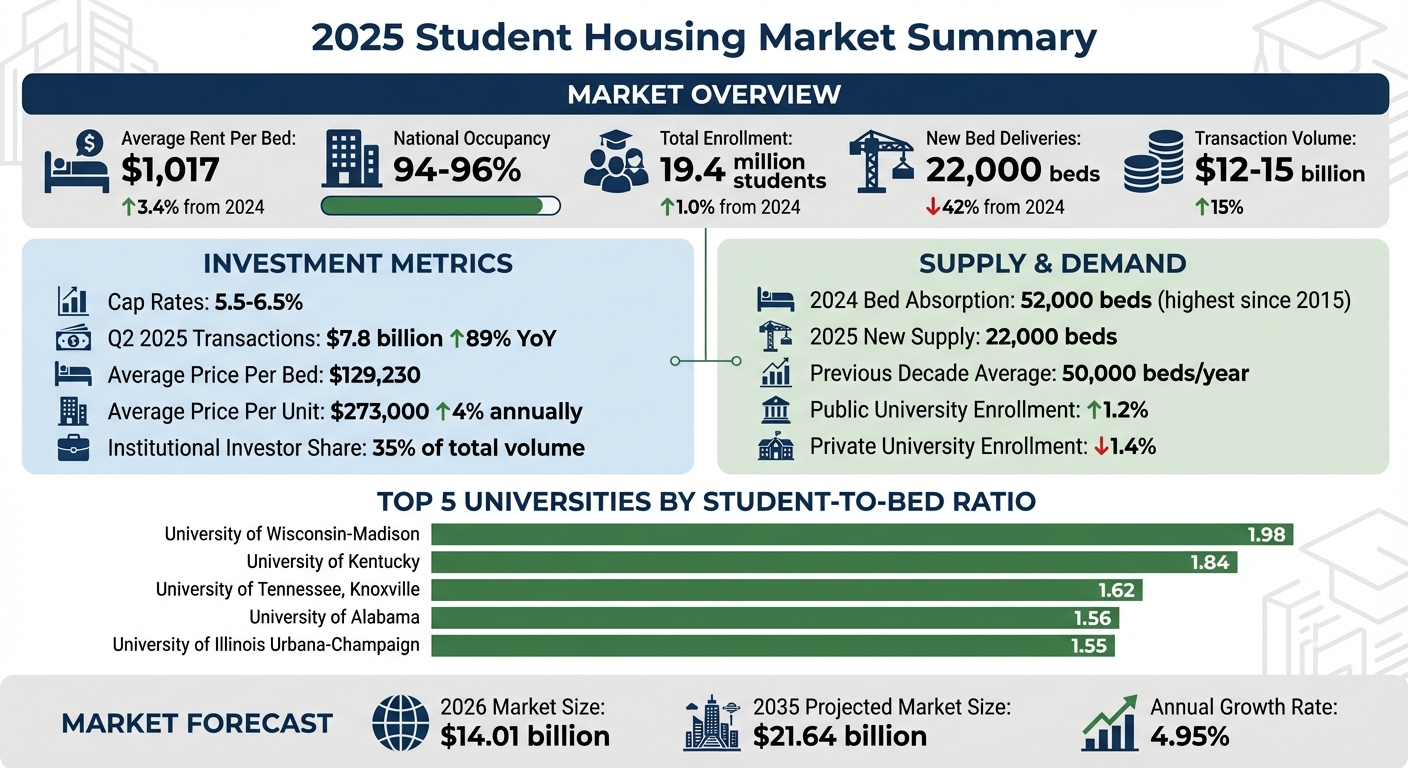

- Rent Growth: Average rent per bed increased by 3.4% to $1,017, following significant rises in 2023 and 2024.

- Occupancy Rates: National rates stabilized at 94-96%, with leading markets like Atlanta and Austin exceeding 97%.

- Enrollment Growth: U.S. college enrollment reached 19.4 million, up 1% from 2024, driven by public universities in the South and Midwest.

- Supply Drop: New bed deliveries fell by 42% compared to 2024, with only 22,000 beds added due to rising construction costs and labor shortages.

- Investment Surge: Transaction volumes grew 15% to $12–15 billion, with cap rates tightening to 4.8–5.5% in core markets.

These trends highlight a constrained market with increasing investor interest, particularly in flagship public universities and secondary markets.

2025 Student Housing Market Key Metrics and Performance Indicators

2025 Performance Metrics

Rent Growth and Occupancy Rates

In 2025, the national average asking rent per bed climbed to $1,017, marking a 3.4% increase after jumps of 9% in 2023 and 6% in 2024. This steady growth continues to outperform the broader multifamily market [2].

"Though rent growth has slowed from previous years, it still outpaces the broader multifamily sector." – Cushman & Wakefield [2]

Flagship public universities reported an occupancy rate of 91.6% as of September 2025, reflecting localized supply-demand mismatches [2]. Preleasing for the 2025–2026 academic year kicked off at record speeds, with rates reaching 47.1% by December 2024 - up 7.4 percentage points from December 2023 [1]. Leading markets like the University of Alabama and the University of Kentucky set the tone, achieving prelease rates of 96.8% by May 2025 and 97.2% by June 2025, respectively [4]. To entice early commitments, landlords offered concessions averaging 8.5% of asking rent per bed, applied to 36.2% of beds [3].

These indicators reflect the solid performance that continues to support cap rate stability.

Cap Rates and Market Conditions

Cap rates for student housing remained steady, ranging between 5.5% and 6.5% throughout 2025. These rates generally ran 25 to 50 basis points higher than those for conventional multifamily properties [5]. Over the 12 months ending in Q2 2025, the national cap rate compressed by 10 basis points, signaling increased confidence among investors [4]. Properties within 0.5 miles of campus commanded a 33% premium compared to those farther away [2].

Investment activity surged as institutional capital poured into the student housing sector. By Q2 2025, $7.8 billion in transactions had taken place - an 89% increase year-over-year. Institutional investors accounted for 35% of total volume, with capital shifting away from struggling office assets [4]. Valuations reflected this momentum, with the average price per bed reaching $129,230 over the 12 months ending in October 2025 [2]. Similarly, transaction pricing averaged $273,000 per unit in Q2 2025, up 4% annually [4]. A standout example of institutional interest was KKR's $1.64 billion portfolio acquisition in 2025, further solidifying the sector's appeal [4].

sbb-itb-99d029f

Supply and Demand Analysis

New Bed Deliveries Drop 42%

The student housing market saw a sharp contraction in its construction pipeline in 2025, with only 22,000 new beds delivered - a 42% drop compared to the 38,000+ beds added in 2024 [3]. This is a significant shift from the annual average of 50,000 beds delivered during the previous decade [5].

The slowdown stems from a mix of economic and industry-specific challenges. Tariff increases in mid-2025 on steel, aluminum, HVAC systems, and machinery parts doubled construction costs per bed [3]. On top of that, tighter bank lending, labor shortages, and rising insurance premiums further complicated new developments. Additionally, concerns over the rise of online education during the pandemic delayed many projects [4].

"The sharp pullback in the 2025 pipeline is no coincidence - it's a clear sign of growing caution mounting across the industry." – RealPage [3]

Despite the slowdown in new construction, the reduced supply has led to favorable market conditions. Occupancy rates for purpose-built student housing at RP 175 universities reached 96.2% in 2024 [3], and the limited supply has helped sustain rent growth. This supply-demand imbalance, coupled with steady enrollment numbers, sets the stage for a closer look at regional trends.

Enrollment Growth by Region

U.S. college enrollment hit 19.4 million students for the Fall 2025 semester, a 1.0% increase from the previous year and the highest level since 2018 [5]. However, regional trends reveal varying pressures on student housing markets.

The South and Midwest have seen the most enrollment growth, especially at large public universities. Public university enrollment rose by 1.2%, while private institutions experienced a 1.4% decline [5]. The 20 largest universities reported average enrollment growth of 3.5%, outpacing the 2.4% growth seen at smaller schools [3]. This concentration of enrollment growth in specific areas has intensified housing demand in certain regions.

Southern and Midwestern universities now report the highest occupancy rates, a reversal of pre-pandemic trends when institutions in the Northeast and West led the market [3]. This shift reflects both changing demographics and the increasing appeal of flagship state schools over smaller private colleges.

Absorption Rates and Supply Shortages

With strong enrollment and limited new construction, the market's ability to absorb demand is under strain. In 2024, 52,000 beds were absorbed - the highest level since 2015 - while only 22,000 new beds were delivered in 2025, exacerbating the national housing shortage [3].

The shortage is most acute in high-demand markets. For instance, the University of Wisconsin-Madison has a student-to-bed ratio of 1.98, meaning nearly two students compete for every available purpose-built bed [4]. Similarly, the University of Kentucky and the University of Tennessee, Knoxville show ratios of 1.84 and 1.62, respectively [4]. These figures underscore the growing gap between available housing and enrollment, particularly at flagship universities where demand is surging.

| University | Undergraduate Demand | Total Bed Supply | Student-to-Bed Ratio |

|---|---|---|---|

| University of Wisconsin-Madison | 35,399 | 17,876 | 1.98 |

| University of Kentucky | 25,586 | 13,932 | 1.84 |

| University of Tennessee, Knoxville | 30,564 | 18,843 | 1.62 |

| University of Alabama | 34,389 | 22,100 | 1.56 |

| University of Illinois Urbana-Champaign | 37,140 | 23,923 | 1.55 |

Source: Matthews™ [4]

Development Trends in 2025

Smart Technology in New Buildings

By 2025, smart technology has become a must-have in student housing developments [7]. Features like keyless entry, automated climate control, and energy monitoring are now standard, offering residents the convenience of adjusting lighting, sound, and temperature through smartphone apps. These tools not only simplify daily life for students but also make property management more efficient [6][7][8].

Beyond convenience, smart technology is helping students create personalized environments. Adjustable lighting, sound dampening, and climate settings allow residents to tailor their spaces to individual study habits or sensory preferences, promoting wellness and comfort [8]. This shift highlights the growing focus on student-centered design that aligns with modern leasing trends.

Flexible Leasing and Privacy Features

In 2025, students are making more deliberate choices about housing, with affordability and specific amenities driving decisions [9]. Flexible leasing models have emerged as a direct response to supply challenges, offering options that better fit student budgets. Multi-bedroom units are particularly popular, as they balance private spaces with shared costs. For example, rental rates for 3-bedroom units rose 6.9% year-over-year, while 5-bedroom units saw a 6.1% increase. On the other hand, demand for studios and 1-bedroom units has dropped, with pre-leasing activity declining by 3.2% and 2.9%, respectively [9].

To offset rising rental costs, landlords are offering concessions on an average of 8.5% of beds, covering 36.2% of the market [3]. As College House notes, “Higher rental rates coupled with lower pre-leasing figures suggest that students may be more selective, with affordability and amenities playing an increasing role in decision-making” [9].

Sustainability and Wellness Features

Student housing in 2025 prioritizes wellness and sustainability, with privacy now seen as a key factor in supporting mental health rather than an optional luxury [6][7][8]. Developers are designing spaces that cater to diverse needs, including quiet areas for neurodivergent students, who make up 15%–20% of the population [8]. Features like natural lighting, sensory-controlled environments, and flexible spaces encourage both social interaction and personal retreat.

Sustainability remains a cornerstone of new developments. Common features include LED lighting, smart thermostats, energy-efficient appliances, low-flow water fixtures, and EV charging stations [7]. However, rising costs have added pressure to construction budgets, with mid-2025 tariffs doubling expenses for steel, aluminum, and HVAC systems. Coastal developments also face higher insurance premiums [3].

Some universities are finding creative ways to manage these rising costs. At San Diego State University, the "Evolve" project is delivering 3,600 units by streamlining construction phases and using early rental income to fund later stages, saving $80 million and cutting delivery time in half [8]. Similarly, California State University-Sacramento’s Mt. Whitney Hall, set to open in Fall 2026, will house 335 students in spaces designed to promote wellness and connection [8]. As Samuel Jones, Associate Vice President for Campus Life at Sacramento State, puts it:

"At Sacramento State, we believe that every student deserves more than just a place to live; they deserve a place to belong... supporting the whole student by creating spaces that promote connection, wellness, and the freedom to just be themselves" [8].

These innovations not only enhance student living but also integrate seamlessly with urban planning strategies.

Urban Infill and Mixed-Use Projects

Urban infill projects have taken center stage in 2025, focusing on locations near campuses to provide walkable, community-oriented housing options. These developments align with students’ growing demand for convenience and integration with campus life. The trend also reflects a broader market shift toward multi-functional spaces that combine living, learning, and social engagement.

For instance, Purdue University’s "Varcity at Purdue" project in West Lafayette, Indiana, blends student and senior housing, fostering intergenerational connections through mentoring programs while emphasizing community and accessibility [8]. Similarly, Worcester Polytechnic Institute’s Foisie Innovation Studio & Residence Building merges 40,000 square feet of classrooms and maker spaces with housing for 140 students, creating a dynamic Living Learning environment [8].

These mixed-use projects highlight the evolving expectations of students, who now seek housing that supports both academic success and meaningful social experiences beyond traditional dormitory models.

Investment and Development Forecast

Market Growth Through 2035

The market is projected to grow steadily, expanding from $14.01 billion in 2026 to $21.64 billion by 2035, with an annual growth rate of 4.95% [4]. This growth is fueled by institutional investors redirecting their capital from struggling sectors like office real estate to more stable, recession-resistant assets.

In Q2 2025, annual transaction volume hit $7.8 billion, marking an impressive 89% year-over-year increase [4]. Kyle Matthews, CEO of Matthews™, sheds light on this trend:

"With the office sector in particular facing significant headwinds, an increasingly larger share of the capital allocated for U.S. real estate is being directed toward niche sectors like student housing" [4].

Investment is particularly focused on flagship public universities, especially those in Power Five athletic conferences such as the Big Ten and SEC. While the number of U.S. high school graduates peaked in 2025 and is expected to decline by up to 13% by 2041, Southern states like Texas, Florida, and Tennessee are anticipated to buck this trend, maintaining strong demand [3][5].

These dynamics have laid the groundwork for an increase in public-private collaborations.

Public-Private Partnership Activity

Public-private partnerships (P3s) are playing a significant role in addressing the housing shortages at flagship universities, accounting for 30% of new projects [4]. At the University of Wisconsin–Madison, for instance, the student-to-bed ratio is 1.98, meaning nearly two students vie for every one purpose-built bed [4].

Such partnerships allow universities to tackle housing deficits without overburdening their budgets. For example, the University of Tennessee, Knoxville, experienced record enrollment of 38,728 students in 2024, leaving a housing shortfall of over 11,700 beds. In response, major developers like Landmark Properties announced large-scale projects in early 2025, targeting the market's 1.62 student-to-bed ratio [4]. Similarly, Florida State University is set to lead the nation in new student housing supply for Fall 2026, with over 2,600 beds scheduled for delivery [10].

Jonathan Rivera, Director at Capright, highlights the strategic focus on these areas:

"Demand is increasingly concentrated around large flagship public universities, particularly in growth regions such as the southern United States" [5].

This trend aligns with enrollment patterns and the financial stability of public institutions. Public university enrollment grew by 1.2% in 2025, while private colleges saw a 1.4% decline [5].

Beyond flagship universities, secondary markets are also presenting promising opportunities.

Secondary Market Opportunities

Smaller cities in the Sun Belt region are emerging as attractive investment destinations, particularly in underserved university markets with growing student populations. Cities like Lexington, KY, and Knoxville, TN, are delivering strong returns due to rapid enrollment growth and limited housing inventory [10]. For example, the University of Kentucky has a student-to-bed ratio of 1.84 and reported a 94.0% pre-leasing rate as of mid-2025. Meanwhile, the University of Tennessee is expected to expand its purpose-built housing inventory by over 40% between 2025 and 2026 [4][10].

These secondary markets often present advantages that larger metropolitan areas cannot. Kyle Matthews underscores this point:

"The most compelling investment opportunities are not defined by the absolute size of a university's student body, but rather by the structural imbalance between student housing demand and available supply" [4].

National cap rates for student housing range between 5.50% and 6.50%, typically 25–50 basis points higher than conventional multifamily properties, making them appealing to investors [5]. With the average price per unit at approximately $273,000 as of Q2 2025 and national average rents ranging from $912 to $915 per bed, these markets offer both strong immediate returns and potential for long-term growth [4][5].

Using CoreCast for Student Housing Analysis

Market Data Tracking with CoreCast

For investors in student housing, keeping an eye on rent trends, occupancy rates, construction pipelines, and competitor activity is essential. CoreCast simplifies this process by offering real-time market metrics, historical data, and mapping tools that reveal supply-demand imbalances.

Access to historical data is a game-changer for understanding market shifts. For instance, users can analyze the 42% drop in new bed deliveries projected for 2025 and evaluate how this tightening supply might influence their investment strategies. This often involves performing scenario analysis to prepare for various market outcomes. With national average rents at $1,017 per bed and occupancy rates holding steady at 91.6%, having accurate, up-to-date insights ensures that investment decisions are based on solid ground.

Beyond tracking market trends, CoreCast also enhances deal execution and portfolio management, making it a comprehensive tool for investors.

Portfolio and Deal Management

CoreCast’s pipeline tracker is designed to handle every stage of a student housing deal, from underwriting to closing. Whether investors are targeting established university hubs or exploring opportunities in secondary markets, the platform provides advanced tools for portfolio analysis across various regions.

The stakeholder center takes communication to the next level, streamlining interactions with partners. With branded reporting features, investors can create polished, customized reports that highlight key portfolio performance metrics, tailored to meet the needs of specific stakeholders.

By consolidating these features, CoreCast reduces inefficiencies, allowing investors to focus on strategy rather than juggling multiple tools.

End-to-End Platform Benefits

Instead of piecing together separate tools for underwriting, market research, and investor relations, CoreCast offers a fully integrated platform. Investors can underwrite deals, track them through the pipeline, analyze their portfolios, and generate detailed stakeholder reports - all within one system.

This unified approach makes it easier to compare markets side by side without switching between platforms. While CoreCast integrates seamlessly with property management systems to ensure smooth data flow, its primary focus is on delivering powerful investment insights - not on handling daily property operations or bookkeeping tasks. This sharp focus ensures that investors have everything they need to make data-driven decisions efficiently.

Evolution of the Student Housing Market: Product & Trends | Webinar

Conclusion

The 2025 student housing market continues to grapple with a persistent mismatch between supply and demand, creating notable opportunities for investors. Key indicators paint a picture of a robust yet supply-limited market. National occupancy rates stand at 96.2%, while new bed deliveries have fallen sharply - dropping 42% to just 22,000 beds [3]. At the same time, U.S. college enrollment has surged to 19.4 million, the highest since 2018. Much of this demand is concentrated at large public flagship universities, particularly within the SEC and Big Ten conferences [4]. These institutions highlight the stark gap between available housing and student needs. As Kyle Matthews, CEO of Matthews™, aptly stated:

"The persistent imbalance between the number of students seeking to live near campus and the number of available beds creates a favorable operating environment" [4].

Investment activity has surged in response, with transaction volumes hitting $7.8 billion by mid-2025 - an impressive 89% increase compared to the previous year [4]. However, challenges loom on the horizon. Rising construction costs, ongoing labor shortages, and tariffs are expected to further constrain new supply. Additionally, a 22% year-over-year decline in F-1 visas and enrollment struggles at smaller institutions add layers of uncertainty [3][5]. Despite these hurdles, pre-leasing for the 2026–2027 academic year shows strong momentum, reaching 52.3% by March 2026, up from 45.6% the year prior [5].

For investors, the ability to adapt to these dynamics will be key. Data-driven strategies, supported by tools like CoreCast, offer critical real-time insights and portfolio analysis, making it easier to navigate both flagship and secondary markets. With cap rates ranging from 5.50% to 6.50% and average asking rents at $915 per bed, understanding local market trends is essential to unlocking growth opportunities [5].

While the sector offers structural advantages, success will depend on careful analysis of factors like enrollment patterns, regional housing supply, and shifting demand. Investors who embrace integrated analytics platforms and focus on high-demand flagship university markets will be best positioned to make the most of the opportunities ahead.

FAQs

What markets are most likely to see the biggest rent increases in 2026?

Large university towns with growing student enrollments and limited housing options are expected to see notable rent hikes by 2026. These areas, often recognized as key college housing markets, tend to have a mismatch between demand and supply, creating conditions that benefit property owners.

How can I tell if a university market is truly supply-constrained?

A student-to-bed ratio exceeding 1.5 signals a shortage of housing, meaning there are more students than available beds. This often leads to higher rents and full occupancy. Additional signs of tight supply include high pre-leasing rates - like 93.7% recorded in August 2025 - and occupancy levels hitting or surpassing 95%. These trends are particularly evident in areas where new housing construction is slowing or development pipelines are shrinking, with a notable 42% decline in 2025.

What should I watch to gauge student housing investment risk in 2025–2026?

To evaluate the risks tied to student housing investments for the 2025–2026 period, it's essential to zero in on a few critical factors. Pay attention to enrollment trends, as shifts in student populations can directly impact demand. Keep an eye on regional demand changes, which may vary depending on location-specific factors. Occupancy rates are another key metric, offering insight into how well properties are performing. Additionally, monitor rental price stability to gauge whether the market can sustain consistent returns. Lastly, consider construction activity, as new developments can affect supply and competition. These elements play a major role in understanding market dynamics and making smarter investment decisions.