How Inflation Affects Real Estate Investments

Inflation changes the game for real estate investors. It can increase costs for construction, maintenance, and financing while raising property values and rental income. To navigate this, you need to understand both the challenges and opportunities:

- Challenges: Higher construction costs, rising interest rates, and tenant affordability issues can shrink profit margins. Conducting scenario analysis can help you prepare for these market shifts.

- Opportunities: Property values often grow faster than inflation, and fixed-rate mortgages reduce debt's real cost over time. Plus, landlords can adjust rents to match inflation.

Key Takeaways:

- Rising costs can strain budgets, but real estate remains a solid hedge against inflation.

- Long-term ownership and fixed-rate loans protect investments as inflation erodes money's value.

- Choosing the right properties and using effective performance tracking strategies is essential.

Inflation shifts wealth toward asset owners. By understanding its effects and applying smart strategies, you can protect and grow your portfolio.

How Inflation Impacts Real Estate Investments: Challenges vs Opportunities

How to Use Inflation to Your Advantage with Real Estate

sbb-itb-99d029f

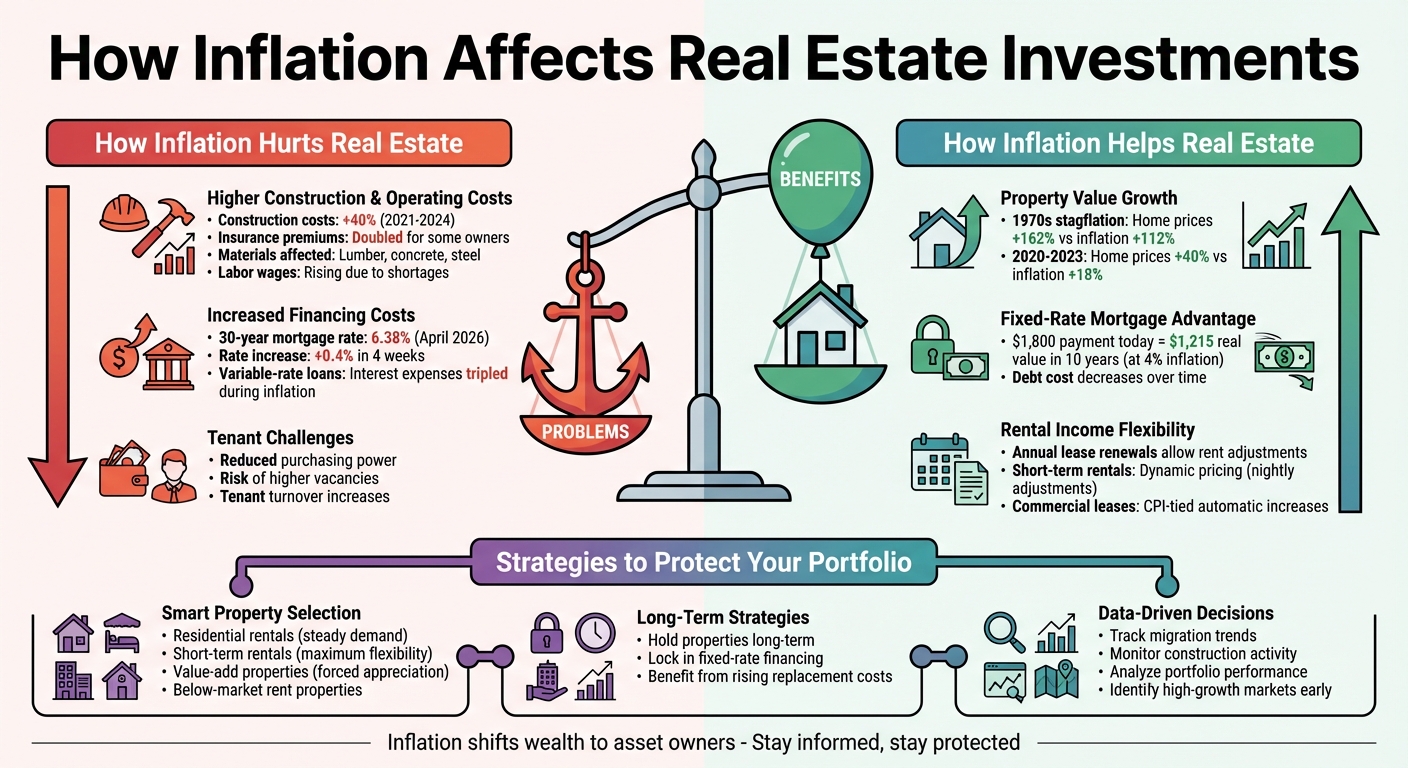

Problems: How Inflation Hurts Real Estate Investments

Inflation can open doors for new opportunities, but it also brings a host of challenges. Rising costs in construction, maintenance, and financing can squeeze profit margins, forcing real estate investors to rethink how they approach their portfolios.

Higher Construction and Operating Expenses

Inflation significantly increases costs tied to both building and maintaining properties. From 2021 to 2024, construction costs jumped by 40% as the prices of essential materials like lumber, concrete, and steel skyrocketed [3]. On top of that, labor shortages have pushed wages higher for contractors and maintenance teams. Everyday operational costs - such as property taxes, utility bills, and routine upkeep - also climb as service providers adjust their fees to match inflation. Even insurance premiums have doubled for some property owners due to higher replacement values [3].

Arie van Gemeren, CFA, captures this challenge succinctly:

"When inflation runs hot, but your expenses rise faster than your rents, you get margin compression." [3]

And it’s not just about operating costs. Rising financing expenses add another layer of difficulty for investors.

Increased Interest Rates and Financing Costs

Central banks typically raise interest rates to curb inflation, and this directly impacts borrowing costs. As of April 1, 2026, the 30-year fixed mortgage rate hit 6.38%, up by 0.4% in just four weeks [2]. For investors using variable-rate loans, the situation can be even more dire - interest expenses have been known to triple during inflationary periods [3]. These higher borrowing costs are slowing down new property acquisitions and putting pressure on cash flow for existing investments that were once profitable.

Tenant Payment Challenges and Reduced Demand

Inflation doesn’t just affect property owners - it also impacts tenants. Rising costs for essentials like groceries, gas, and utilities reduce tenants' purchasing power. As renters have less disposable income, their ability to handle rent increases diminishes. This puts landlords in a tough spot: raising rents to cover rising costs could lead to higher vacancies and frequent tenant turnover. Even fully leased properties face risks if rent hikes push tenants beyond what they can afford.

These factors combined highlight the delicate balancing act required to navigate real estate investments during inflationary times.

Benefits: How Inflation Can Help Real Estate Investors

Inflation might seem like a hurdle for many, but for real estate investors, it can actually open up some strategic opportunities. While rising costs and financing challenges are real, inflation has historically worked in favor of those who manage and benchmark real estate portfolios wisely. Over time, real estate has shown its strength as a tool for building wealth, even when prices are climbing.

Real Estate as Protection Against Inflation

When inflation drives up construction costs, property values often rise alongside them. This means that existing properties typically gain value. For instance, during the 1970s stagflation, U.S. home prices surged by 162%, outpacing the cumulative inflation rate of 112% [4][1]. A more recent example: between 2020 and 2023, national home prices jumped 40%, compared to an 18% cumulative inflation rate [2].

Fixed-rate mortgages also become a powerful advantage during inflationary periods. As the value of the dollar decreases, the real cost of a fixed monthly mortgage payment shrinks over time. To illustrate, a $1,800 mortgage payment today would feel like just $1,215 in ten years if inflation averages 4% annually [2]. Unlike gold, which may hold its value but doesn’t generate income, real estate offers both capital appreciation and monthly cash flow [2].

This combination of value growth and income generation makes real estate a standout choice for preserving wealth and staying ahead of inflation.

Ability to Raise Rents

One of the key benefits for landlords during inflation is the flexibility to adjust rents. Residential leases are typically renewed annually, giving property owners the chance to align rents with current market rates. For short-term rental owners, platforms like Airbnb make it even easier to respond to inflation, as dynamic pricing tools allow for nightly rate adjustments [2].

This adaptability ensures that rental income keeps pace with rising costs, such as property taxes, insurance, and maintenance. Similarly, commercial property owners with leases tied to the Consumer Price Index (CPI) benefit from automatic rent increases tied directly to inflation. This built-in mechanism helps sustain cash flow, even as operating expenses climb.

Solutions: How to Protect Your Portfolio from Inflation

Inflation can be a tough challenge, but real estate investors have tools to safeguard their portfolios. By choosing the right types of properties, focusing on long-term strategies, and leveraging market insights, you can counter rising costs and financing pressures while preserving the value of your investments.

Focus on Property Types That Thrive During Inflation

Not all properties react the same way to inflation. Residential rentals, like single-family homes and small multifamily units, tend to hold up well because housing demand remains steady. Plus, annual lease renewals give landlords the chance to adjust rents in line with inflation. Short-term rentals, such as those listed on Airbnb or VRBO, offer even more flexibility. Since these leases aren’t locked in for long periods, owners can quickly adapt to market changes.

Another option? Value-add properties. Renovating older units not only boosts their appeal but also creates forced appreciation. Additionally, rising replacement costs can drive natural market appreciation. Acquiring properties with below-market rents can be another smart move - this approach allows you to benefit from an existing discount while leaving room for rent increases in the future. To make these strategies even more effective, pair them with fixed-rate financing. This way, the real value of your debt decreases over time as inflation erodes the dollar’s purchasing power [2].

Hold Properties Long-Term for Growth

Long-term ownership is a powerful ally in inflationary times. Fixed-rate loans mean your repayment amounts stay consistent, even as the value of money declines. Meanwhile, rising construction costs make new developments pricier, which can increase the market value of existing properties [2][4]. Combining steady rental income with capital appreciation makes holding properties a reliable way to hedge against inflation.

Stay Informed with Real-Time Data

To make these strategies work, you need accurate and timely market data. Platforms like CoreCast provide insights into trends like population growth, migration, and construction activity - factors that directly impact property values and rental demand [2]. With tools like these, you can identify high-growth markets before they become saturated. CoreCast also offers features to track deals, analyze portfolio performance, and visualize properties alongside competitive landscapes. By using such data-driven tools, you can adapt your strategies to changing market conditions, ensuring your portfolio stays resilient against inflation [2].

Conclusion

Inflation brings its share of hurdles and opportunities for real estate investors. On one hand, rising construction costs, higher interest rates, and tenant payment challenges can put pressure on portfolios. On the other, real estate consistently proves to be one of the strongest hedges against inflation. Historical trends show that property values often grow faster than inflation rates, making it a reliable asset class during uncertain times.

To succeed in inflationary markets, investors need a combination of smart property selection, long-term holding strategies, and accurate market insights. For example, focusing on flexible, value-add residential properties, securing fixed-rate financing, and leveraging up-to-date market data can help safeguard and grow your portfolio. But these strategies are only effective when backed by dependable market intelligence.

That’s where platforms like CoreCast come into play. CoreCast provides tools to track migration trends, monitor construction activity, analyze portfolio performance, and map out competitive landscapes. This allows investors to pinpoint high-growth areas early. The platform also offers features like portfolio audits to ensure rents align with market rates, equity calculators for unlocking hidden value, and guidance on securing optimal long-term financing.

Inflation tends to shift wealth from those holding cash to those owning assets. With accurate, real-time data, you can position yourself to benefit from this shift. Whether it’s adjusting rents, updating insurance to reflect rising replacement costs, or locking in contractor rates before costs climb further, having the right insights is crucial.

The most successful investors stay ahead by being informed and proactive, using real-time market intelligence to adapt and thrive.

FAQs

Is real estate still a good inflation hedge in 2026?

Real estate continues to be a solid option for hedging against inflation in 2026. Historically, property values and rental income tend to rise in step with inflation, allowing investors to maintain their purchasing power. This characteristic makes real estate an effective way to safeguard wealth during periods of economic uncertainty.

Should I choose a fixed-rate or adjustable-rate loan during inflation?

During times of inflation, opting for a fixed-rate loan can be a smart move. It secures your interest rate, protecting you from any future hikes in borrowing costs. On the other hand, an adjustable-rate loan might seem appealing initially but could become pricier as interest rates climb.

Which property types hold up best when prices rise?

Multi-family properties tend to excel in periods of rising prices. Why? They offer the opportunity for more frequent rent adjustments. This adaptability enables property owners to counteract inflation's impact and keep their income streams consistent.