Emerging Industries Driving Healthcare Facility Demand

The healthcare real estate market is transforming. Four industries - telehealth, ambulatory surgical centers (ASCs), biotech and life sciences, and wellness-focused preventive care - are reshaping facility demand. These sectors emphasize smaller, specialized spaces and patient convenience over traditional hospital setups. Here's a quick breakdown:

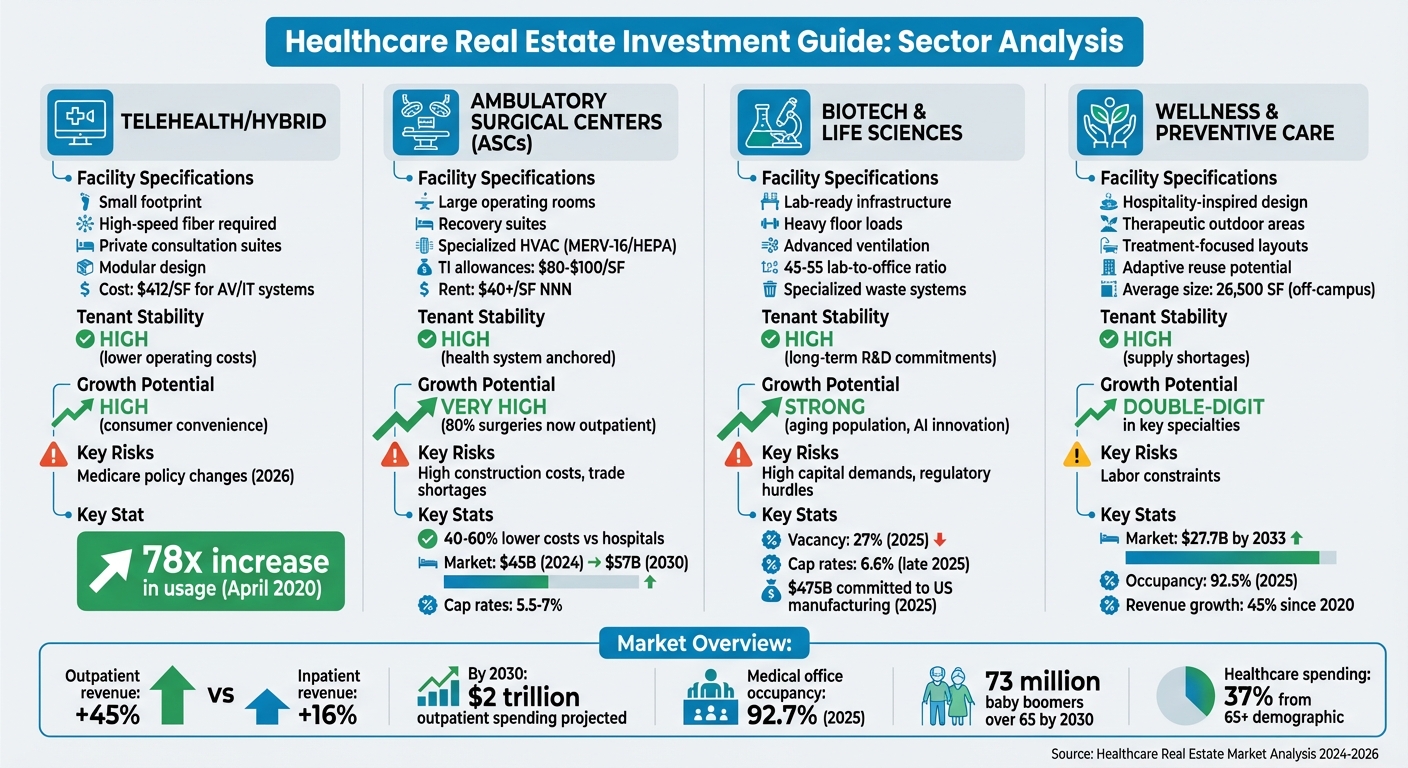

- Telehealth: Requires private, tech-enabled spaces with strong cybersecurity. Medicare policy changes in 2026 could impact growth.

- ASCs: High demand for suburban outpatient hubs with advanced surgical infrastructure. Offers cost savings for patients and payers.

- Biotech and Life Sciences: Needs highly specialized labs and manufacturing facilities. Growth driven by aging populations and AI innovations.

- Wellness and Preventive Care: Focuses on patient-centered designs and off-campus locations, blending healthcare with hospitality.

Key Stats:

- Outpatient revenue surged 45% since 2022, far outpacing inpatient growth (16%).

- By 2030, outpatient healthcare spending could hit $2 trillion, driven by an aging population.

- Medical office building occupancy reached 92.7% by 2025.

Investors should prioritize real estate investment and asset management intelligence to understand sector-specific needs, like telehealth's modular designs or ASCs' advanced surgical setups, to navigate this rapidly shifting market.

1. Telehealth

Facility Requirements

Telehealth facilities demand private consultation spaces equipped with high-quality video conferencing systems and secure data solutions. These setups rely on high-speed internet, advanced telecom networks, and strong cybersecurity measures to ensure HIPAA compliance [1]. By 2026, the average cost for outfitting medical outpatient facilities, including high-intensity AV/IT systems, reached $412 per square foot [9].

Modern facility designs are leaning toward modularity, featuring movable walls, multipurpose areas, and specialized zones like pharmacy command centers. Retrofitting with AI-driven systems and smart operations enhances patient flow and maximizes space efficiency [4][6][10]. Strategic location planning also plays a vital role, prioritizing digital connectivity and patient accessibility.

Location Preferences

Telehealth is moving care delivery away from large hospitals to smaller, community-focused facilities. These spaces are often part of high-density, mixed-use developments, chosen for their strong broadband access and proximity to public transportation [1].

"939 Ellis Street is perfectly positioned for providers who need immediate access to hospital systems, public transit, and city and suburban population. It checks all the boxes for modern medical delivery." – Kurt Hackett, Vice President of Asset Management, Rethink Capital [11]

Investment Trends

Investors are increasingly drawn to tech-enabled healthcare portfolios and smaller outpatient clinics that support hybrid care models [1][2]. By the first half of 2025, digital-health platforms accounted for about 60% of healthcare M&A activity, even though only 5% of organizations had achieved full digital maturity by early 2026 [2][3].

The growing popularity of medical coworking spaces - like ShareMD Suites and Clinicube - reflects the demand for flexible, telehealth-ready environments. These spaces offer on-demand clinical suites through membership models [10]. With AV/IT systems and specialized fit-outs driving up costs, involving cost management experts early in the process has become essential for successful project execution [9].

Growth Drivers

Telehealth usage skyrocketed - rising 78-fold in April 2020 [1][11] - and continues to thrive due to its convenience and cost-efficiency [1][7]. AI integration is also helping address healthcare labor shortages, extending the capacity of limited frontline staff [6].

However, challenges loom on the horizon. Medicare provisions for telehealth and hospital-at-home programs are set to expire in early 2026 [2]. Analysts estimate this could result in a loss of 12 million telehealth appointments annually as emergency-era policies phase out [11]. Additionally, some specialties, such as orthopedics and cardiology, are pulling back from virtual-first care due to clinical limitations and shifting insurance reimbursements that favor in-person visits [11].

The evolving telehealth landscape highlights the need to adapt infrastructure and policies to sustain its growth while addressing emerging challenges. This shift also sets the stage for examining trends in other healthcare sectors.

sbb-itb-99d029f

2. Ambulatory Surgical Centers (ASCs)

Facility Requirements

ASCs are built with specialized infrastructure to meet the demands of modern surgical care. These facilities require advanced HVAC systems with MERV-16 or HEPA filtration, negative pressure rooms for isolation procedures, and UV-C light systems for ongoing disinfection. Dedicated medical gas lines, reliable backup power, and high-speed internet for electronic health records are also essential [12].

To accommodate advanced procedures like orthopedic robotics and joint surgeries, ASCs now include larger operating rooms. The lead times for critical equipment, such as sterilization systems and imaging devices, can range from 30 to 40 weeks [13]. Infection control is a priority, with facilities incorporating seamless, non-porous surfaces, copper-alloy antimicrobial materials, and surgical-grade flooring. Touchless technology, like sensor-activated doors and faucets, adds another layer of sterility.

These infrastructure requirements shape the strategic decisions behind site selection, which we’ll explore next.

Location Preferences

While telehealth focuses on digital connectivity, ASCs need physical spaces optimized for surgical workflows. Increasingly, ASCs are being developed in high-growth suburban areas where patient access is easier, and operational costs are lower. For example, in April 2025, Sutter Health committed $800 million to create a centralized outpatient hub in Santa Clara, California [16].

Another trend is repurposing vacant retail spaces into surgical centers, which allows for quicker market entry and reduced development costs. ASCs are often integrated into multi-specialty Medical Office Buildings (MOBs), enhancing referral networks and streamlining patient services. Developers are targeting areas with aging populations and high numbers of insured patients, focusing on specialties like orthopedics and cardiology [15].

Investment Trends

By late 2024, United Surgical Partners International (USPI), part of Tenet Healthcare, had expanded its network to 518 ASCs and 25 surgical hospitals across 37 states. The company plans to add 10–12 new centers in 2025, supported by a $250 million annual investment fund for acquisitions [16]. ASC cap rates, ranging from 5.5% to 7%, highlight their appeal as long-term investments [12].

Rising construction costs are driving a shift toward retrofitting existing structures instead of building new facilities. For instance, Novant Health is working on a 25-center ASC network as of early 2026, focusing on moving lower-acuity cases - like orthopedics, ophthalmology, and gastroenterology - out of hospitals to improve efficiency and access [17]. The U.S. ASC market, valued at $45 billion in 2024, is projected to grow to $57 billion by 2030 [14].

Growth Drivers

ASCs benefit from both strong investment activity and significant cost advantages. Operating at 40% to 60% lower costs than traditional hospitals, they are attractive to payers and patients alike [12][18]. Outpatient knee replacements saw a 293% increase between 2019 and 2023, fueled by advancements in minimally invasive techniques and anesthesia [18]. Adding to this momentum, the Centers for Medicare & Medicaid Services (CMS) approved a 2.6% payment increase for ASCs in 2026 and expanded the ASC Covered-Procedures List to include more complex procedures like cardiac ablation [4][19].

"In 2026, the biggest driver will be the continued shift of high-acuity procedures into the ASC setting. Payers, employers and patients all want value, and ASCs are uniquely positioned to deliver that without sacrificing quality." – Steve Hockert, Chief Development Officer, Solara Surgical Partners [19]

Technological advancements are also transforming the field. Robotics and AI are enhancing surgical precision and decision-making. As Neil Manug, Senior Director of Business Development, aptly said:

"Robotics are to the surgeon's hands as AI is to the surgeon's brain" [14]

With roughly 10,000 baby boomers turning 65 daily, demand for musculoskeletal and gastrointestinal care continues to grow [20].

3. Biotech and Life Sciences

Facility Requirements

Biotech and life sciences facilities demand infrastructure that goes well beyond standard lab setups. Think advanced mechanical systems with HVAC redundancy, high-capacity power, and precise environmental controls as non-negotiable basics [21]. Interestingly, AI-driven biotech firms are reshaping the game by favoring a 45–55 lab-to-office ratio, leasing about a third less space per employee compared to traditional biopharma companies [10,25].

However, converting office spaces into labs often falls short of meeting the technical needs. Common issues include narrow hallways, poorly located loading docks, uneven floors, vibrations, and ceilings that are too low [21]. As Liz Berthelette, Head of Northeast Research & National Life Science Research at Newmark, puts it:

"Lab users are focused on spaces that fit their scientific needs like a glove, and they are ignoring spaces that aren't quite the perfect fit or would require any construction or extreme modifications" [21].

Biomanufacturing facilities require even more specialized designs. These Class A facilities are critical for reshoring pharmaceutical production, a trend that saw a 185% increase in demand for biomanufacturing space during the first half of 2025 [23].

Location Preferences

When choosing locations, biotech companies prioritize three things: proximity to research institutions, access to specialized talent, and availability of venture capital. Unsurprisingly, core hubs like Boston-Cambridge, the Bay Area, and San Diego dominate, holding 78% of life sciences inventory owned by REITs or private investors [24]. These areas also benefit from massive NIH funding, with over $500 billion projected between 2024 and 2034 [25].

Secondary markets such as New Jersey, Philadelphia, and Raleigh-Durham are gaining momentum as cost-friendly options, especially for biomanufacturing. For instance, in the third quarter of 2025, AI-focused biotech firms like Lila Sciences and Neuralink signed large-scale leases ranging from 150,000 to 200,000 square feet, reflecting a shift in demand beyond traditional research hubs [21].

Investment Trends

In 2025, global pharmaceutical companies committed $475 billion to U.S. manufacturing and R&D [22]. Yet, the market is undergoing a correction, with national lab vacancy rates hitting 27% in 2025, up by 20.4 percentage points in just three years [10,29]. This oversupply has created a tenant-friendly market, where only the highest-quality, purpose-built facilities are attracting leases.

Cap rates for life sciences properties rose to 6.6% by late 2025, compared to a low of 4.4% in early 2022 [24]. Meanwhile, the construction pipeline has shifted focus, with 63% of new space pre-leased as of late 2025, emphasizing build-to-suit projects over speculative developments [26]. Still, the oversupply issue looms, with 18.7 million square feet of lab space expected to be repurposed by 2030 [10,25].

Growth Drivers

The biotech sector’s growth is being propelled by an aging U.S. population, which is driving demand for new medications and treatments for chronic diseases [27,31]. At the same time, AI is revolutionizing drug discovery and clinical trials, reshaping how companies use their spaces. Mark Bruso, Director of Boston and National Life Sciences Research at JLL, highlights this shift:

"The integration of artificial intelligence into life sciences is fundamentally altering the physical infrastructure requirements of the entire industry. AI-native companies are pioneering new models of space utilization that emphasize computational power, automation and flexible laboratory configurations" [22].

Another key driver is the push for domestic manufacturing, as companies look to strengthen U.S. supply chains in response to global trade tensions. Biomanufacturing facilities are thriving, with occupancy rates above 90%, outperforming traditional R&D labs [24]. AI-native biotech firms now make up one-sixth of all biotech venture capital deals, steering facility designs toward computational spaces and data centers rather than conventional wet labs [10,31].

These ongoing changes in biotech and life sciences set the stage for exploring how wellness and preventive care shape healthcare facility demand next.

4. Wellness and Preventive Care

Facility Requirements

Wellness centers are embracing designs inspired by hospitality, focusing on comfort and aesthetics to enhance the patient experience. These modern facilities feature calming interiors, therapeutic outdoor areas, and inviting waiting spaces. But it’s not just about looks - spaces are being reconfigured to prioritize treatment areas over administrative ones, maximizing revenue-generating square footage[27].

To meet the demands of specialized services like IV therapy, cryotherapy, and hormone optimization, facilities are upgrading their infrastructure. They’re also incorporating advanced imaging equipment and integrating technology, such as telehealth suites, AI-driven patient flow systems, and enhanced power and cooling setups to support these innovations[6].

Tanya Hart, Commercial Real Estate Leader at Colliers, highlights this shift:

"Specialty healthcare real estate is shifting from administrative-heavy layouts to patient-first, revenue-optimized environments."[27]

Location Preferences

The wellness sector is leading the charge in decentralizing healthcare. Around 80% of new medical outpatient buildings are now being constructed off-campus, often in residential and retail areas to prioritize convenience for patients. These off-campus locations average about 26,500 square feet, significantly smaller than the 66,900-square-foot facilities typically found near hospitals[7].

Developers are also creatively repurposing vacant retail spaces - like former pharmacies and mall anchor stores - into multifunctional hubs that combine urgent care, diagnostics, and behavioral health services[7]. Younger generations are particularly drawn to transit-friendly and mixed-use developments that offer a blend of health and lifestyle services in one location[28].

Investment Trends

Investment in wellness facilities is booming, reflecting the sector's rapid growth. The medical spa and wellness destination market is expected to hit $27.7 billion by 2033, with an annual growth rate of 14.7%[27]. Outpatient revenue has soared 45% since 2020, far outpacing the 16% growth of inpatient services. This has driven medical outpatient building occupancy to 92.5% by 2025, with some regions exceeding 95%[3].

Triple-net asking rents reached $24.86 per square foot in Q2 2024, while tenant improvement allowances for full buildouts now range from $80 to $100 per square foot - an increase of $10 to $15 compared to pre-pandemic levels[8,6]. Behavioral health and psychiatry services are also in high demand, accounting for 18% of leased outpatient building space in 2024[8].

Growth Drivers

The aging U.S. population is a major factor shaping the wellness industry. By 2030, 70 million Americans - 20% of the population - will be 65 or older, a group responsible for 37% of healthcare spending. This demographic shift is expected to push outpatient healthcare spending to nearly $2 trillion. Additionally, outpatient visits per patient have risen from 1.8 in 2000 to 2.4 in 2022[7].

Shifting patient behavior is another key driver. As Tanya Hart explains:

"Patients now proactively invest in mental, physical, and aesthetic health."[27]

This proactive mindset is fueling demand for services that blend self-care with traditional medicine. Notably, healthcare real estate investment trust (REIT) returns outperformed all other major property types - such as multifamily, industrial, retail, and office - over the year leading to August 2025[7].

These trends underscore the growing emphasis on decentralized, patient-centered care, which is redefining the wellness and preventive care landscape.

Healthcare Real Estate Trends and Capital Markets with Seth Gilford, Vice President, Healthcare...

Advantages and Challenges by Industry

Healthcare Real Estate Investment Comparison: 4 Emerging Sectors

This breakdown highlights the main advantages and challenges each healthcare sector presents for real estate investors. Each segment offers a mix of opportunities and risks that shape investment decisions and portfolio growth.

Telehealth facilities have smaller physical footprints and lower operating costs, making them appealing. However, they demand significant upfront investments in high-speed fiber, advanced cybersecurity measures, and HIPAA-compliant infrastructure. Additionally, shifts in Medicare policy represent a major risk factor[2].

Ambulatory Surgical Centers (ASCs) stand out for their strong financial returns. Rents often exceed $40 per square foot NNN, and tenant stability is high since health systems depend on these centers for high-margin procedures. For instance, a gallbladder operation costs roughly $2,200 in an ASC compared to $12,000 in a hospital[7]. On the downside, construction costs are steep, with tenant improvement (TI) allowances now ranging from $80 to $100 per square foot. Furthermore, shortages of skilled trades can lead to significant project delays[5][31].

Biotech and life sciences facilities require highly specialized spaces, including heavy floor loads, advanced ventilation systems, and robust power capacity. These facilities often enjoy stable tenancy due to long-term R&D commitments and the use of specialized equipment. However, the high capital requirements and complex regulatory landscape can be challenging for investors[30].

Wellness and preventive care centers are experiencing rapid growth, particularly in specialties like psychiatry and endocrinology. These facilities often incorporate hospitality-inspired designs that enhance patient loyalty. Despite their growth potential, labor shortages remain a significant hurdle[7].

Each sector's specific demands influence investment strategies, as shown in the table below:

| Industry Sector | Facility Specifications | Tenant Stability | Growth Potential | Key Risks |

|---|---|---|---|---|

| Telehealth/Hybrid | Small footprint; high-speed fiber; private suites; modular design | High (due to lower operating costs) | High (driven by consumer convenience) | Medicare policy changes[2] |

| ASCs | Large ORs; recovery suites; specialized HVAC; $80–$100/SF TI allowances | High (anchored by health systems) | Very High (80% of surgeries now outpatient)[10] | High construction costs; trade shortages[31] |

| Biotech/Life Sciences | Lab-ready; heavy floor loads; advanced ventilation; specialized waste systems | High (long-term R&D commitments) | Strong (aging population, innovation) | High capital demands; regulatory hurdles[30] |

| Wellness/Behavioral | Hospitality-inspired designs; nature elements; adaptive reuse potential[10][29] | High (supply shortages)[29] | Double-digit growth in key specialties[2] | Labor constraints[7] |

"Outpatient growth, demographic strength, and resilient MOB fundamentals continue to attract diversified capital." – Jordan Selbiger, Executive Vice President of U.S. Healthcare Capital Markets at Colliers[3]

The healthcare real estate market is appealing due to its stability and demographic-driven growth. However, investors need to carefully assess factors like infrastructure demands, regulatory risks, and construction timelines to make informed decisions about emerging sectors. These considerations are crucial for navigating the complexities of this evolving market.

Conclusion

The healthcare real estate market is evolving, with four key sectors leading the charge: Telehealth, Ambulatory Surgical Centers (ASCs), Biotech and Life Sciences, and Wellness and Preventive Care. While each sector presents unique opportunities, ASCs and wellness facilities are emerging as the most promising in the near term. Consider this: over 80% of surgeries now occur in outpatient settings, and patients save an average of 59% when procedures are done in ASCs instead of hospitals [10][7]. On the other hand, the demand for behavioral health services is skyrocketing, fueled by the fact that one in four U.S. adults faced mental health challenges in 2021 - far outpacing the available supply [29].

These trends are underpinned by shifting demographics. By 2030, 73 million baby boomers will be over 65, with 10,000 reaching retirement age every single day [10]. Despite making up just 17% of the population, this group accounts for 37% of total healthcare spending [7]. With healthcare expenditures expected to surpass 20% of the U.S. GDP by 2033, the demand for specialized and efficient facilities will only grow [5].

"Healthcare real estate has matured into a core investment asset - one positioned for sustained relevance and growth." – Healthcare Real Estate Insights [5]

For investors, the focus should be on high-margin ambulatory facilities located in fast-growing suburban areas, especially those supporting specialties like endocrinology, psychiatry, and oncology [2][4]. The ongoing shift toward decentralized care models, the transformation of retail spaces into healthcare hubs, and the integration of AI in facility management are reshaping how and where healthcare is delivered. Success in this space will depend on understanding each sector’s infrastructure needs, navigating regulatory hurdles, and managing construction timelines effectively.

In this fast-moving market, having access to real-time data is crucial. Tools like CoreCast (https://corecastre.com) offer a comprehensive solution, providing insights to evaluate specialized healthcare assets, track pipeline deals across sectors, and conduct advanced portfolio analyses - all in one platform. This streamlined approach equips investors to make quicker, data-driven decisions in a competitive landscape where speed and precision are critical.

FAQs

Which emerging sector requires the least space but the most tech investment?

Telehealth doesn't require much in terms of physical space, but it does demand a solid investment in technology. It depends on advanced digital and telecommunication tools to provide healthcare services. By cutting down on the need for traditional facilities, telehealth shifts the focus to building a strong tech infrastructure.

What should I check first when buying or building an ASC property?

The first step is to carefully evaluate the location. Make sure it aligns with the demand for outpatient care, population growth trends, and any local regulations. Pay close attention to certificate-of-need restrictions, which are enforced in some states and can directly affect whether development is even possible.

Why are life sciences labs hard to convert from office buildings?

Life sciences labs are particularly difficult to transform from standard office buildings due to their need for highly specialized infrastructure. These facilities require advanced mechanical, electrical, and plumbing systems to support their operations. On top of that, features like clean rooms, vivariums, and negative-pressure rooms add even more layers of cost and complexity to the conversion process.