Predictive Analytics for CRE Insurance Risk

Predictive analytics is transforming commercial real estate (CRE) insurance by using data-driven tools like AI for risk profiling, satellite imagery, and IoT sensors to predict risks and improve decision-making. Traditional methods relying on manual inspections and ZIP code-based pricing are being replaced with advanced techniques that evaluate risks at the building level. This shift enables faster underwriting, more accurate pricing, and better portfolio management.

Key takeaways:

- Advanced Risk Detection: Tools like aerial imagery and IoT sensors identify issues such as roof damage or water pooling before they lead to claims.

- Data-Driven Insights: Historical claims, geospatial data, and real-time monitoring provide detailed property-level risk profiles.

- Efficiency Gains: AI reduces underwriting timelines and automates claims processing, saving time and cutting costs.

- Portfolio Protection: Predictive models help insurers and property owners anticipate disasters and reduce unexpected expenses.

For insurers and property owners, adopting predictive analytics is no longer optional - it’s essential for staying competitive in a rapidly evolving market.

AI, Predictive Modeling, and Data Trends in Underwriting

sbb-itb-99d029f

Data Sources for CRE Insurance Risk Modeling

Predictive analytics in commercial real estate (CRE) insurance draws from three primary data sources: historical records, geospatial and climate data, and real-time IoT data. Together, these layers bring precision to risk forecasting, shifting the industry from broad ZIP code-based assessments to detailed building-level analysis.

Historical Claims and Property Data

Historical claims and property data form the backbone of predictive models. Essential details include building age, location, construction type, square footage, and occupancy type. More advanced models also consider specifics like roof material and age, window resistance, sprinkler systems, and exposure to hazards [4][7].

These granular insights are key to refining rates and managing risks. For instance, in June 2025, an underwriter used batch analytics on a policy for a grocery store chain. The analysis flagged one location with 74% pavement degradation and 75% poor illumination. Properties with such conditions often have double the loss ratios, prompting the underwriter to adjust rates and mandate resurfacing before renewal [2]. Additionally, tools like Natural Language Processing (NLP) transform unstructured data - claims notes, adjuster narratives, and emails - into structured insights. This process extracts sentiment and keywords, which can help identify high-severity claims early [6].

Geospatial and Climate Data

Geospatial and climate information adds another layer of precision to risk evaluation. These models analyze factors like elevation, proximity to water, nearby fault lines, and defensible space (distance to vegetation) to assess vulnerabilities to floods, wildfires, and other hazards. The ULI CRE Guide highlights over 50 data points tied to environmental risks that can be factored into underwriting [5].

In September 2025, CNA Financial Corporation combined satellite imagery and vector data (including seismic lines and property boundaries) with proprietary datasets in Google Cloud's BigQuery. This integration revealed subtle elevation changes and firebreak locations, enhancing risk assessments for properties in disaster-prone areas [7].

"Geospatial AI can help insurers move past outdated regional risk models to perform property-level precision analysis, allowing them to identify good, insurable risks in climate-exposed markets their competitors have abandoned" – Christina Lucas and Denise Pearl, Google Cloud [7]

IoT and Real-Time Monitoring

IoT devices and satellite imagery provide real-time property data, enabling insurers to take proactive measures. Sensors tracking temperature, humidity, pressure, and vibration offer insights into asset longevity and potential breakdown risks, going far beyond traditional evaluation methods.

Real-time monitoring supports "Predict & Prevent" strategies, allowing insurers to address hazards before they lead to losses. For example, a commercial building owner can install water sensors for around $6,000 to help avoid damages that typically cost $75,000 [8]. In September 2025, a technology provider began using AI to analyze near real-time imagery, identifying street-level risks like standing water from poor drainage or debris at culverts. This approach offers a more detailed view of flood risks than static flood zone maps [7]. Insurers using AI and real-time data in underwriting have reported up to a 5% improvement in loss ratios and expense savings of 10% to 15% [9]. These advancements give insurers a sharper edge in optimizing underwriting decisions.

How Predictive Analytics Works in CRE Insurance

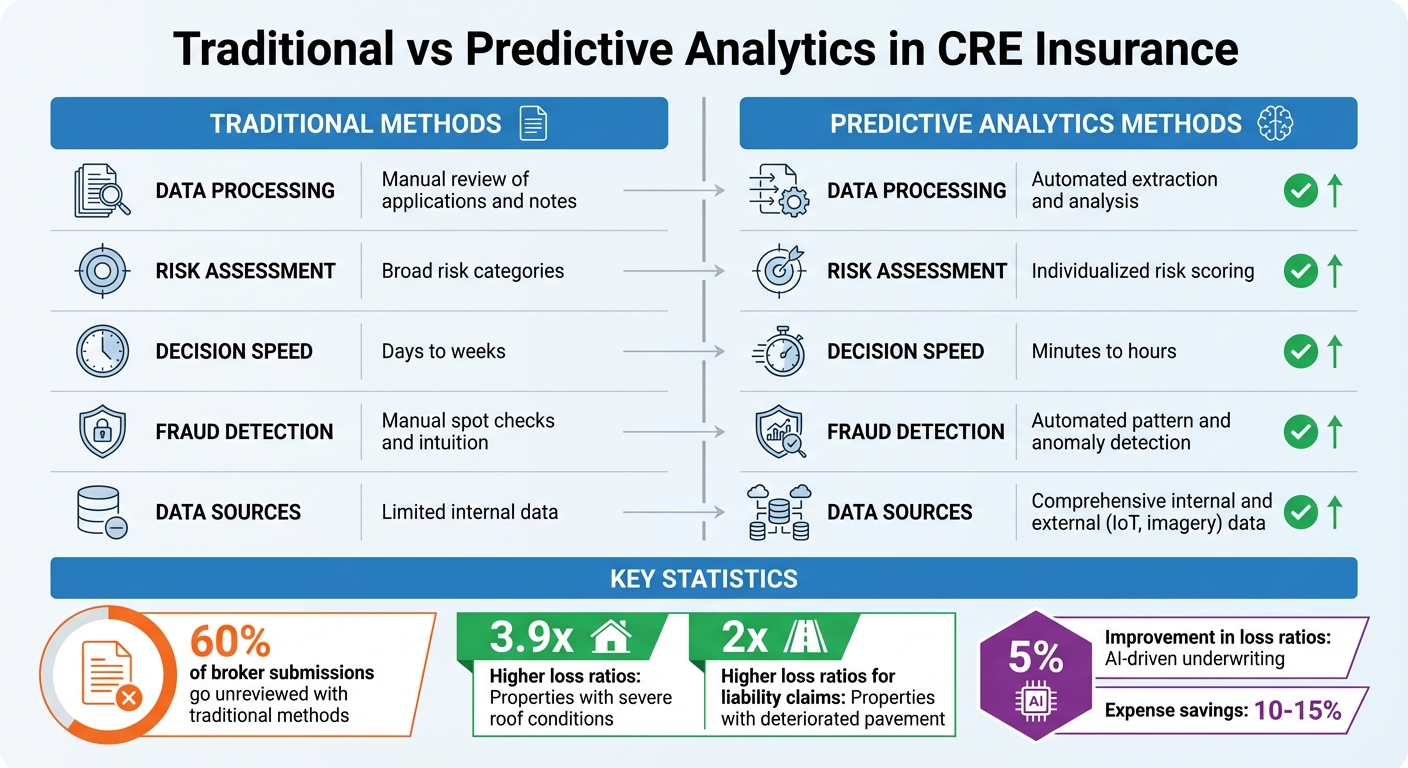

Traditional vs Predictive Analytics in CRE Insurance Claims Processing

Predictive analytics transforms raw data into practical insights through methods like property-level risk scoring, catastrophe modeling, and fraud detection. These tools analyze vast amounts of data at once, shifting insurance decisions from reactive approaches to proactive strategies.

Risk Scoring for Individual Properties

Today's risk scoring examines properties on an individual basis, moving away from the outdated practice of relying solely on ZIP code data. These systems consider factors like property features, tenant creditworthiness, lease terms, and physical conditions to create a composite score. This score helps determine whether a property should be fast-tracked for approval or flagged for rejection [10].

Condition-aware underwriting takes this a step further by using high-resolution aerial imagery and AI to spot physical risks that traditional methods might miss. For example, properties with roofs rated as "severe" show 3.9 times higher loss ratios than those in "excellent" condition. Similarly, buildings with deteriorated pavement experience double the loss ratios for liability claims [2]. These detailed insights allow insurers to assess individual buildings more accurately, even in areas typically considered high-risk, avoiding blanket rules like rejecting all properties over 30 years old [4].

Risk scoring isn't just for initial evaluations - it plays a role in ongoing portfolio management and stress testing. These systems achieve 70% to 85% accuracy in predicting investment outcomes. CRE investors using them report 25% to 35% fewer unexpected costs and tenant defaults compared to those relying on traditional methods [10].

Beyond assessing individual risks, predictive analytics also enhances catastrophe forecasting and fraud detection.

Catastrophe Modeling and Loss Forecasting

Catastrophe (CAT) models have advanced significantly, moving from ZIP-code-level analysis to square-foot-level precision [4]. Modern tools incorporate secondary factors like roof quality, equipment stability, window impact resistance, and wind or hail exposure. These details refine Average Annual Loss (AAL) and Probable Maximum Loss (PML) projections.

"Secondary characteristics are becoming the differentiator in modeling data. These are what sway average annual loss and probable maximum loss projections." – Marshall Heron, National Real Estate Practice Leader, Risk Strategies [4]

Take Honeycomb Insurance as an example. This digital-first MGA uses AI and proprietary remote inspection data to assess risks at the building level in 20 states. By analyzing factors like hail exposure and historical loss trends, they can offer coverage in high-risk areas where many insurers have pulled out [4]. This targeted approach helps insurers identify profitable opportunities in markets others might overlook.

Real-time data integration further improves forecasting. Predictive CAT models draw on satellite imagery, live weather updates, and IoT sensors to estimate potential losses and allocate resources proactively [6]. Insurers can even reach out to policyholders in high-risk areas before disasters strike, helping reduce the severity of claims.

Fraud Detection and Claims Processing

Predictive analytics also plays a key role in identifying fraudulent claims and speeding up the claims process. Machine learning uncovers unusual patterns in claims data, such as geographic clusters, suspicious timing (e.g., claims filed right after a policy starts), or inconsistencies in documentation [11]. Fraud in non-health insurance costs the U.S. industry over $40 billion annually [6].

These systems analyze the First Notice of Loss (FNOL) to predict how complex or severe a claim might be. Claims are then routed to the right adjuster or specialized team for faster handling [11][6]. AI can even estimate a claim's total cost early on, helping insurers set accurate financial reserves and adjust them as new information comes in [11][6].

Using Natural Language Processing (NLP), unstructured text from claims notes, emails, and adjuster reports is converted into structured data. This helps flag keywords or sentiments linked to high-severity or potentially fraudulent claims [6]. Low-complexity claims that meet certain criteria can be "fast-tracked", resolving them quickly without manual investigation [11][6].

| Aspect | Traditional Claims Method | Predictive Analytics Method |

|---|---|---|

| Data Processing | Manual review of applications and notes | Automated extraction and analysis [11] |

| Risk Assessment | Broad risk categories | Individualized risk scoring [11] |

| Decision Speed | Days to weeks | Minutes to hours [11] |

| Fraud Detection | Manual spot checks and intuition | Automated pattern and anomaly detection [11] |

| Data Sources | Limited internal data | Comprehensive internal and external (IoT, imagery) data [11] |

This shift to automated processing addresses a major bottleneck: around 60% of broker submissions in commercial lines go unreviewed due to slow, manual workflows [2]. By automating these processes, insurers can capture missed opportunities while improving speed and accuracy throughout the claims lifecycle.

Benefits for CRE Insurers and Property Owners

Predictive analytics is reshaping how risks are assessed and managed, offering a more precise and efficient approach to insurance and property protection. By moving away from manual processes, it brings clarity and value to every stage of the insurance lifecycle.

Better Risk Understanding and Pricing

With advanced data collection tools, predictive analytics now allows for a much more detailed look at risks. Instead of using broad metrics like ZIP codes, insurers can evaluate properties at the building level, factoring in details like roof condition, window durability, and equipment safety measures. For example, properties with deteriorating pavement face double the loss ratios for liability claims, while poorly maintained roofs are linked to higher loss rates [4][2].

"The future of commercial property insurance is hyper-differentiated. Blanket underwriting is gone. The carriers and MGAs who can assess risk at the square-foot level, not the ZIP code level, are the ones who will write profitably." – Itai Ben-Zaken, CEO, Honeycomb Insurance [4]

This level of detail benefits both insurers and property owners. Older, well-maintained properties can secure competitive rates, while hidden risks in newer buildings are flagged early. Properties using geospatial insights, for instance, see 7.3% higher annual returns, and investors relying on advanced analytics achieve 4-5% higher risk-adjusted returns compared to market averages [12].

Automated tools also help insurers create dynamic risk profiles by analyzing tenant demographics, historical claims, crime rates, and property details. These profiles enable flexible pricing that accounts for various risk scenarios, such as natural disasters or tenant defaults, reducing the chances of over- or under-insurance [13]. IoT sensors further enhance this process by detecting issues like water leaks or HVAC malfunctions before they escalate into costly claims [13].

Faster Underwriting and Decision-Making

Predictive analytics doesn’t just make risk assessment more accurate - it also speeds up the underwriting process. AI-driven platforms can now analyze high-resolution aerial images to instantly score property conditions, cutting underwriting timelines from weeks to just hours. This lets insurers quickly approve low-risk properties while dedicating more attention to complex cases [2].

Renewals are also streamlined. Batch processing allows underwriters to evaluate entire portfolios at once, automatically identifying which policies are ready for auto-renewal and which need further review. By embedding predictive scores directly into underwriting systems, decisions can be made in real-time without the need for manual data entry [2].

The financial benefits are substantial. McKinsey's 2025 Global Insurance Report highlights that 60% of a commercial carrier's financial performance now hinges on operational efficiency rather than the specific lines of business they write [2]. By 2030, AI is expected to save the real estate industry $34 billion through efficiency gains [1]. Additionally, in 2025, 9 out of 10 organizations view AI as a key strategy for gaining a competitive edge [1].

Stronger Portfolio Protection

Predictive analytics also plays a critical role in protecting entire portfolios by identifying risks before they become problems. Through scenario simulations - such as natural disasters or market corrections - insurers and property owners can proactively address vulnerabilities. This might involve reinforcing infrastructure or adjusting leasing strategies to mitigate potential losses [3].

Early detection tools, like fault-detection sensors, help prevent costly claims. For example, identifying HVAC issues in 22 units saved one property owner over $120,000 in potential leasing losses and emergency repairs [14].

Tenant retention also benefits. Predictive models can analyze lease data and CRM interactions to pinpoint tenants likely to leave. By offering targeted incentives, property managers have increased retention rates from 72% to 87% and reduced unexpected turnover from 28% to 13% [14]. For insurers, stable occupancy reduces risk and creates more predictable loss ratios across their portfolios.

These advancements showcase the comprehensive risk management capabilities that platforms like CoreCast can deliver, providing seamless solutions for insurers and property owners alike.

How CoreCast Supports CRE Insurance Risk Management

CoreCast provides a powerful, all-in-one platform designed to streamline insurance risk management for commercial real estate (CRE). By integrating precise analytics, CoreCast tackles the issue of fragmented data often seen in insurance assessments. Accurate predictive analysis requires evaluating a wide range of factors, such as building age, construction type, roof materials, electrical systems, historical claims, crime rates, flood zones, wildfire risks, and contamination history [16]. CoreCast consolidates all this information into a single platform, eliminating the need for insurers to work with incomplete or scattered data.

Data Aggregation and Pipeline Tracking

Traditional insurance due diligence often leans on rough estimates provided by brokers, which can lead to inaccuracies. CoreCast changes the game by aggregating property records, market trends, and third-party data into one seamless interface. Its pipeline tracking for CRE ensures continuous updates throughout the underwriting process, shifting from static, one-time evaluations to ongoing risk monitoring. This approach is versatile, supporting underwriting for diverse asset types - from stabilized office buildings to development projects - making it easier to assess properties with varying risk profiles [16]. This unified system not only enhances efficiency but also lays the groundwork for deeper portfolio analysis and competitive insights.

Portfolio Analysis and Competitive Mapping

CoreCast's portfolio analysis tools help pinpoint properties that disproportionately drive up insurance costs. For example, AI risk scoring can uncover cases where just three properties account for 60% of a portfolio's overall risk due to issues like aging roofs or outdated electrical systems [16]. The platform allows users to visualize these risks, prioritize upgrades to lower insurance costs, and track the financial impact of these improvements. Its mapping feature adds another layer of insight by showing properties in relation to competitive assets and geographic risks, such as wildfire-prone or flood-risk areas. With this data, AI-driven portfolio modeling can help reduce insurance expenses by 8–15% through smarter, data-informed coverage adjustments [16]. These insights directly influence underwriting strategies, enabling more precise and effective risk management.

AI-Driven Automation and Reporting

CoreCast leverages AI to provide continuous risk updates as property conditions change. This is particularly useful for parametric insurance, where AI monitors real-time environmental data to alert property managers when specific triggers are nearing, giving them a chance to take preventive measures before claims arise [16]. Additionally, CoreCast’s customizable reporting tools cater to different stakeholders. For instance, lenders might receive reports focused on portfolio-level risks and coverage adequacy, while property managers get actionable insights on maintenance issues affecting premiums and insurability. This tailored approach is crucial, especially as over 80% of CRE investors emphasize the importance of predictive analytics and business intelligence in decision-making [15].

Conclusion

Predictive analytics is reshaping the landscape of CRE insurance by moving away from outdated, static spreadsheet evaluations to a dynamic, data-driven approach. This shift allows for continuous monitoring, uncovering potential vulnerabilities - like roof membrane damage or pavement wear - before they escalate into costly financial setbacks. For property owners, this means avoiding emergency repairs that can often surpass $50,000 [10].

The numbers paint a clear picture of its impact. Properties with severely deteriorated roofs experience loss ratios nearly 3.9 times higher than those in excellent condition [2]. Meanwhile, investors leveraging AI-driven risk tools report a 25% to 35% reduction in surprise expenses [10]. With U.S. commercial building insurance costs expected to climb nearly 80% by 2030 [17], the ability to proactively identify and address risks isn’t just helpful - it’s becoming a necessity.

To meet these challenges, platforms like CoreCast are stepping in with solutions that consolidate scattered data, automate repetitive processes, and provide real-time insights into property portfolios. By doing so, CoreCast turns insurance risk management into a strategic advantage, seamlessly incorporating the benefits of predictive analytics into a single, comprehensive platform.

"In real estate, the art of the deal is increasingly becoming the science of the data" – Edward Glaeser [12]

The evidence is compelling: firms that utilize geospatial analytics and predictive modeling achieve 4% to 5% higher risk-adjusted returns compared to market averages [12]. As technology advances with tools like IoT and climate risk modeling, the divide between data-savvy firms and those clinging to traditional methods will only grow. Adopting predictive analytics today is the key to building a more resilient and profitable future in CRE insurance.

FAQs

What data do I need to start predictive risk modeling for a building?

To kick off predictive risk modeling for a building, start by gathering precise data about the property's risks and overall performance. Useful sources include historical market trends, tenant behavior, property values, maintenance records, and operational challenges. You can also gain valuable insights from lease agreements, tenant profiles, and data from IoT devices installed on the property. Having detailed, reliable data is essential for accurately forecasting risks such as tenant defaults, unexpected maintenance problems, or changes in market conditions.

How do insurers use IoT sensors and imagery without invading privacy?

Insurers are leveraging IoT sensors and imagery technology to better manage risks in commercial real estate. These sensors gather data on critical aspects such as equipment performance, structural integrity, and environmental factors - all aimed at assessing the overall health of a property rather than tracking personal activity, ensuring privacy remains intact.

Similarly, aerial imagery, whether captured by drones or satellites, plays a key role in evaluating property risks. This includes identifying issues like roof damage or potential fire hazards. Importantly, these tools are designed to focus solely on property-related data, steering clear of personal information to remain compliant with privacy standards.

How can predictive analytics lower premiums without sacrificing coverage?

Predictive analytics is transforming how insurers set premiums, offering a way to lower costs without sacrificing coverage. By diving into historical data, insurers can accurately pinpoint the risk levels of properties, allowing for fairer and more tailored premiums. For instance, it helps identify potential issues like tenant defaults or property wear and tear in commercial real estate, ensuring policies align closely with actual risks.

This method also streamlines claims management, curbs fraudulent claims, and fosters a more efficient and competitive insurance landscape - all while keeping the quality of coverage intact.